Pay equity audits used to be something only large enterprises worried about a compliance exercise run by a dedicated compensation team with access to specialized software and outside legal counsel. That’s no longer the case.

A growing patchwork of state and local pay transparency laws, combined with rising employee expectations around fairness, means that pay equity has become a board-level topic at companies of every size. And unlike many compliance requirements, pay equity exposure doesn’t wait until you’re large enough to have a comp team. It builds quietly in the background in every hiring decision, every promotion, every off-cycle adjustment until it surfaces in an audit, a lawsuit, or an exit interview.

The good news is that a rigorous pay equity audit doesn’t require a dedicated comp function. It requires the right data, a clear methodology, and increasingly the right tools. This guide walks finance leaders through how to run one from scratch.

TL;DR

- Pay equity audits are no longer just a large-company concern — a growing patchwork of pay transparency laws means exposure builds quietly at companies of every size, in every hiring and promotion decision.

- The key distinction is controlled vs. uncontrolled pay gaps. An uncontrolled gap is the raw difference in average pay between groups. A controlled gap adjusts for role, level, tenure, and geography — and that’s what determines legal exposure.

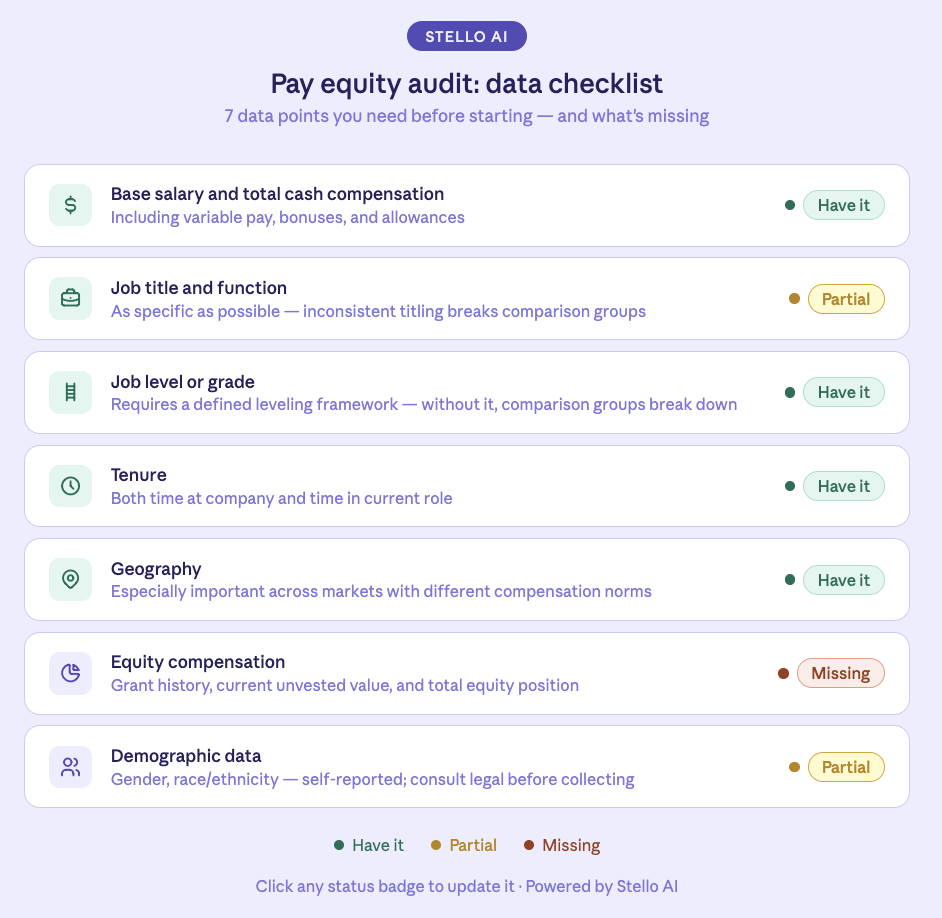

- A rigorous audit requires seven data points: base salary, job title, function, level, tenure, geography, equity compensation, and demographic data. Missing any one of these limits what the analysis can actually conclude.

- The most common obstacle in a first audit isn’t a pay equity problem — it’s a job architecture problem. Inconsistent titling and undefined levels make comparison groups impossible to construct.

- AI changes three things: it flags pay disparities continuously instead of periodically, automates comparison group construction, and integrates equity compensation into the analysis — something most manual audits miss entirely.

- Remediation should happen in the next compensation cycle, not the next annual review. Waiting twelve months to act on a documented gap creates ongoing legal exposure.

- A one-time audit isn’t enough. Pay equity erodes between cycles through new hires, promotions, and off-cycle adjustments — annual audits at minimum, quarterly if tooling supports it.

What a Pay Equity Audit Actually is

A pay equity audit is a structured analysis of compensation data designed to identify whether employees in similar roles, at similar levels, with similar experience are being paid differently — and whether those differences can be explained by legitimate business factors or suggest systemic bias.

The key distinction is between controlled and uncontrolled pay gaps. An uncontrolled gap is the raw difference in average pay between groups — for example, women earning 82 cents for every dollar earned by men across the company. An uncontrolled gap is a starting point, not a finding. It doesn’t account for differences in role, level, tenure, or geography.

A controlled gap — what a pay equity audit actually measures — adjusts for those factors. It asks: among employees doing the same job at the same level with similar tenure, is there a statistically meaningful difference in compensation that correlates with gender, race, or another protected characteristic?

This distinction matters for finance leaders because the controlled gap is what determines legal exposure. A large uncontrolled gap may be fully explained by legitimate factors (more women in lower-paying roles, for example). A small controlled gap — even a few percentage points — may indicate a systemic problem that requires remediation.

Step 1: Assemble Your Data

The foundation of any pay equity audit is clean, complete compensation data. Before running any analysis, pull together the following for every employee:

- Base salary and total cash compensation — including any variable pay, bonuses, or allowances

- Job title and function — as specific as possible

- Level or grade — if you have a job leveling framework, use it here; if not, this is a gap that needs addressing before the audit can be rigorous (we cover why leveling frameworks are foundational in our guide to rolling out a BoxCar program)

- Tenure — both time at the company and time in role

- Geography — especially relevant if you operate across markets with different compensation norms

- Equity compensation — grant history, current unvested value, and total equity position

- Demographic data — gender, race/ethnicity, as self-reported by employees

A note on demographic data: collection practices and legal requirements vary by jurisdiction. Consult legal counsel before collecting or storing this data, particularly if you operate across multiple states or countries.

Step 2: Define Your Comparison Groups

Pay equity analysis requires meaningful comparison groups — sets of employees who are similar enough in role and level that differences in their compensation are worth examining.

The most defensible approach is to use your existing job architecture. If you have defined job families and levels (e.g., “Software Engineer, Level 3”), those become your comparison groups. Employees in the same job family at the same level are the population you analyze for unexplained pay differences.

If your job architecture is inconsistent — job titles that have drifted, levels that mean different things across teams, roles that were created organically without a framework — you’ll need to normalize before you can run a meaningful analysis. This is one of the most common obstacles finance teams hit during a first pay equity audit. The audit surfaces the job architecture problem more than the pay equity problem.

For equity compensation, comparison groups should account for grant date and company stage. An employee who received a grant at Series A and an employee who received a grant at Series C are holding very different instruments, even if the share count looks similar. Comparing raw grant sizes without context produces misleading results.

Step 3: Run the Analysis

With clean data and defined comparison groups, the analysis itself has two layers.

Descriptive analysis: For each comparison group, calculate the average and median compensation by demographic category. Flag any groups where the gap between categories exceeds a threshold — typically 5% for base salary, though thresholds vary. This layer surfaces where to look, not what’s wrong.

Regression analysis: To isolate unexplained pay differences, run a multivariate regression that controls for level, tenure, geography, and performance rating (if available). The residual — the portion of the pay difference not explained by those legitimate factors — is what you’re looking for. If that residual correlates with gender or race at a statistically significant level, you have a finding that requires remediation.

For finance teams without a statistician on staff, this is the step that feels most daunting. In practice, a competent analyst with Excel or basic statistical software (R, Python, or even Tableau) can run the regression. The methodology is well-documented and doesn’t require specialized expertise — it requires data discipline and intellectual honesty about what the results show.

Step 4: Where AI Changes This Process

This is where the gap between what’s theoretically possible and what’s practically achievable for a lean team narrows significantly.

AI-powered compensation platforms change the pay equity audit in three concrete ways.

Continuous flagging instead of periodic audits. A manual pay equity audit is a snapshot — it reflects pay equity at the moment the data was pulled. AI systems that continuously monitor compensation data across the employee population can flag emerging disparities as they develop, rather than waiting for the annual or biannual audit cycle to surface them. A hiring decision that introduces a pay gap in a comparison group gets flagged in weeks, not months.

Automated comparison group construction. Building defensible comparison groups manually — especially across a complex job architecture with inconsistent titling — is time-consuming and judgment-intensive. AI systems trained on job architecture data can normalize titles, map roles to levels, and construct comparison groups automatically, flagging low-confidence matches for human review. What previously took weeks of analyst time takes hours.

Integrated equity analysis. Most pay equity audits focus exclusively on base salary and miss the equity dimension entirely — partly because equity data is harder to pull, and partly because modeling total equity value at the individual level is complex. AI platforms that integrate compensation and equity data can run pay equity analysis across total compensation, not just cash, surfecting disparities that a salary-only analysis would miss entirely. For companies running BoxCar grant programs, where employees may hold multiple overlapping grants at different stages of vesting, this integrated view is particularly valuable. We cover how AI handles this complexity in our guide to AI-powered compensation benchmarking.

Step 5: Remediate and Document

Finding a pay gap is the beginning of the process, not the end. Remediation requires decisions about how quickly to close identified gaps, how to prioritize (largest gaps first, highest-risk roles first, or systematic across the board), and how to communicate changes to affected employees.

A few principles that hold regardless of company size:

Close gaps in the next compensation cycle, not the next annual review. Waiting twelve months to remediate a documented pay gap creates ongoing legal exposure and signals to employees that equity is not actually a priority.

Document the methodology and findings. A written record of the audit methodology, the findings, and the remediation steps is both a compliance asset and a defense document. If a pay equity claim is ever brought, demonstrating that the company conducted a good-faith audit and acted on its findings is meaningful.

Treat it as a recurring process, not a one-time exercise. Pay equity erodes between audits — through promotions, off-cycle adjustments, and new hires who negotiate differently. Building a cadence (annual at minimum, quarterly if tooling supports it) and owning it at the finance and HR leadership level ensures the issue stays managed rather than drifting back.

The Bottom Line

A pay equity audit without a dedicated comp team is not only possible — it’s increasingly necessary. The legal and reputational landscape has shifted to the point where “we don’t have the resources” is not a defensible position for companies of any meaningful size.

The methodology is straightforward. The data requirements are manageable. And AI-powered tooling is closing the gap between what a lean finance team can accomplish and what previously required a specialized function.

The companies that conduct pay equity audits proactively — before a regulator, a plaintiff, or a departing employee forces the issue — are the ones that control the outcome. The ones that wait are the ones that don’t.

FAQs-

1. Do we legally have to conduct a pay equity audit?

It depends on your jurisdiction — some states now require pay equity audits or pay transparency disclosures. But legal requirement aside, documented pay disparities create significant litigation exposure. A proactive audit is cheaper than a reactive one.

2. What’s the difference between a controlled and uncontrolled pay gap?

An uncontrolled gap is the raw difference in average pay between groups. A controlled gap adjusts for role, level, tenure, and geography — and isolates what can’t be explained by legitimate factors. The controlled gap is what determines legal exposure.

3. How long does a pay equity audit take without a dedicated comp team?

For a 50–150 person company with reasonably clean data, expect 2–4 weeks for a first audit — mostly spent normalizing job titles and building comparison groups. With AI tooling, that timeline compresses significantly.

4. What do we do if we find a pay gap?

Close it in the next compensation cycle, not the next annual review. Document the methodology, the finding, and the remediation steps. Waiting twelve months to act on a documented gap creates ongoing legal exposure.

5. How often should we run a pay equity audit?

Annually at minimum — quarterly if your tooling supports it. Pay equity erodes between audits through new hires, promotions, and off-cycle adjustments. A one-time audit that isn’t repeated gives a false sense of compliance.